|

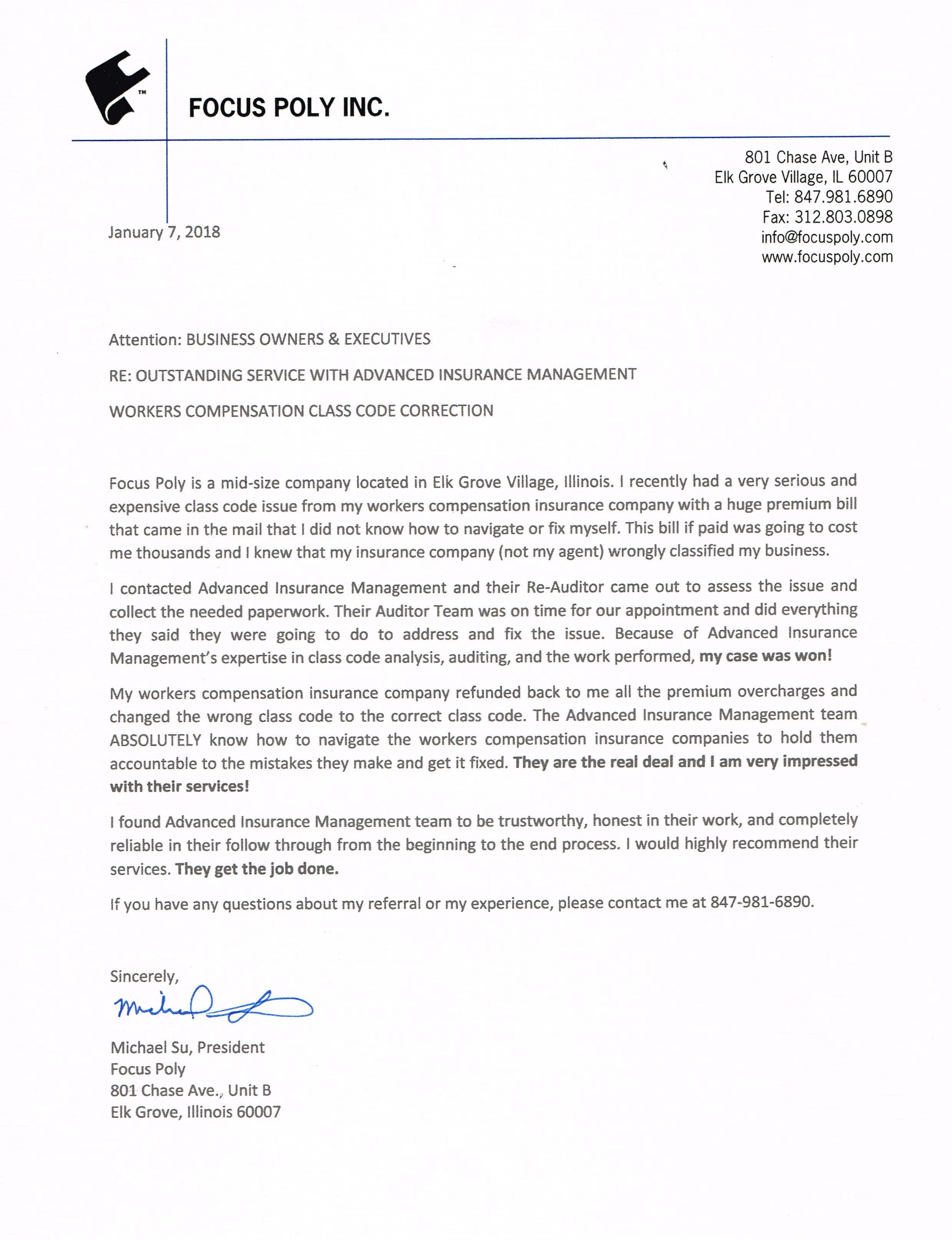

From The AIM Case

Files

We recently received the following letter from a client that

provided a glowing review of our work on their behalf. Take a

look.

speaking of letters...

A

Simple Letter...

...from A.I.M. recently helped a

Chicago-area small manufacturer lower an audit premium demand

from their insurer by about $2,300.00. The insurer had insisted

the additional premium was owed, and cited chapter and verse

from the NCCI manual to support their position. If unchallenged,

this would have cost this company $2,300 every year in

additional Workers Comp premiums.

But our letter pointed out that the insurance company's auditor

had overlooked one very important fact--there was an Illinois

State Special rule that applied to the classification codes in

question, so that the chapter and verse cited by the insurer

earlier didn't apply in this particular instance. And once we

pointed out their error (and dropped a veiled hint that we would

refer the matter to the Department of Insurance if things

weren't corrected) the insurer very nicely said, in effect,

"Oops, our bad."

Helping Particles Accelerate

We recently helped a company that provides technical workers

to a major particle accelerator. They had a major problem--their

experience modifier had risen above 1.00, and that would preclude their

continuing to work on the federal project. Fortunately, AIM was able to

identify and correct problems in the modifier calculation, resulting in reduced

mod calculations and our client being able to continue to help keep those

sub-atomic particles accelerating. You can take a look at the nice letter

they sent us

here.

Keep Those Banners Flying

We just finished helping a small Chicago area manufacturer

of large printed banners and pop-up displays recover $14,000 in Workers Comp

premium overcharges. Their insurance company had made a change in classification

code (to a more expensive class) for their sewing employees. We discovered that

the insurer had failed to give proper notice of this change, and by working with

the Illinois Department of Insurance we were able to get three years worth of

policies corrected, with the resulting premium reduction.

$15,000 Refund for Waste Hauler

Not long ago, we obtained a

$15,000 refund for a waste hauler in Lexington, South

Carolina. The experience modifiers for this client had

been higher than they should have been for several years,

due to the failure of the insurer to properly report Second

Injury Fund reimbursements to NCCI.

A.I.M. got the insurer to file corrected reports, then we

made sure NCCI recalculated those experience modifiers.

Finally, we followed up with the subsequent insurers to get

them to revise audit charges by incorporating those

now-lower experience modifiers.

All in a days work.

The South Carolina Situation

We were commissioned to do a

study a few years ago about how

employers in South Carolina

benefitted (or sometimes didn't) from the operation of that

state's Second Injury Fund. Our study

found that in over 50% of cases where an

employer's insurance company had gotten a

reimbursement from the Fund, the insurance

company hadn't reported the reimbursement

to NCCI, so that the employer's

experience modifier could be lowered.

Now, we're working with individual employers

affected by this problem, to help them recover

those premium overcharges. And so far, we're finding

an even higher percentage of overcharged

employers than we found in the original study.

Even though South Carolina enacted new

legislation to try to address the problem after our

original study was released, it appears that the insurance

industry never bothered to actually

fix the experience mod errors for

all these employers. So now we're making them

fix these overcharges, one employer at a time.

If you're a South Carolina employer that

had a Workers Comp injury reimbursed by the

Second Injury Fund in recent years, you may

well want to have AIM check to see if your

company ever got the experience mod

adjustments you were entitled to. The odds

are that you didn't, and we can do something about

that. Click here

for more information.

|

The Case We Can't Talk About

Sometimes, the results of

our consulting work can't be discussed in any

specifics or detail. That's the case recently,

where AIM consulted with the San

Francisco 49ers football organization

on a Workers Compensation premium matter. The

case was covered by a Confidentiality Agreement,

so we can't disclose anything more than that we

provided consulting services to the 49ers

regarding Workers Compensation premiums, and

that it appears the 49ers were satisfied with

our efforts.

Still, it illustrates that AIM can be of

assistance to a wide variety of employers

regarding Workers Compensation insurance

premiums, even organizations you don't normally

think about in the context of Workers

Compensation insurance.

Helping a

Recycling Company Stay "Green"

Well, we're at

least helping them keep a little more of their

green, as in dollars spent on Workers' Compensation

insurance. Their insurance company, on the

most recent audit, reallocated payroll completely

out of an inexpensive classification, and moved it

all into a much more expensive class. In most

states, there wouldn't be anything that could be

done about such a practice. But in the

particular state where this recycling company is

based, it turns out that the rules are a little

different. Reallocating payroll so completely

that payroll is totally removed from one class and

placed into another is considered the same as a

change in classification, and is prohibited when

it's done late in the term of the policy.

The bottom line is

that A.I.M. reduced the cost of the premium charges

on the audit billing by about $220,000.

An

Exhausting Classification Case

This

Nevada client had recently been inspected by NCCI

and assigned to the Painters code, on the basis that

they used pressure washing equipment to clean

kitchen exhaust vents. NCCI took the position that

the use of pressure washing equipment meant this

company should be assigned the code used for

painting and paperhanging. This change in

classification caused a large increase in manual

rate and premiums for this client. Even worse,

their insurer used this as a basis to change the

prior year's premium charges as well.

Our review found

significant basis for disputing this NCCI decision,

and we assisted the client in preparing a

presentation to the Nevada Workers' Comp appeal

board, which held in the client's favor and returned

them to their original class code. This

enabled the client to avoid the premium increases

for both of the years that their insurance company

was billing them for, as well as avoiding the large

future premium increases that would have resulted

from NCCI's classification change.

The Case of the California

Classification Code

This client was a

printer with operations in both Illinois and

California. And although the Illinois

operations had no recoverable overcharges, it turned

out there was a significant problem with the way

premiums had been computed for the California part

of the company. California's Workers' Comp

premiums are subject to the rules and regulations of

an entirely separate rating bureau. While NCCI

handles such work for most states, California has

the WCIRB. And under WCIRB classification

rules, a different class (and manual rate) applied

for this client's California work, because their

work was to print advertising fliers for grocery

stores--which under California rules, was eligible

for a lower classification than the one used for

other kinds of printing.

We were able to

produce an $85,000 premium reduction for this client

by correcting this problem, and lower all future

premiums for their California operations in the

process.

Unique North Carolina Rule

For a North

Carolina plumber, we found that their experience mod

was higher than it should have been, because of a

unique North Carolina regulation pertaining to

over-reserving of claims. Correcting this

mistake saved this client a fast $5,000 (not all of

our clients are large employers, and not all of our

refunds are huge, but we work just as hard for

smaller clients and smaller refunds as we do for any

other case.)

And Another North Carolina

Case...

For another North

Carolina client, we recently found that they were in

the wrong classification code. The insurance

company had them classed in a paper coating class,

when the client actually mixed chemicals to make

adhesives that third parties then would use to,

among other things, coat paper. Fixing this

mistake saved the client $35,000, and lowered future

premiums as well.

No matter what

state your company operates in, or what kind of work

you do, you might well benefit from a review of your

Workers' Comp charges. You never know what

kinds of overcharges might be hidden in the fine

details.

A Double Whammy

This case

found AIM producing a refund for a plumbing

contractor that totaled over $100,000. The cause of

the overcharges? A combination of miscalculated

experience modifiers and resulting lack of

contractors credit on several policies. You see, if

your company's experience modifier is above a

certain point it disqualifies you from getting a

contractor's credit (which is calculated based on

hourly wages). Correcting the modifiers brought them

low enough for the contractor's credit to come into

play. It took a while to get NCCI to make all the

corrections necessary, and then for the insurance

companies involved to correct their billings and

refund the overcharges, but it was worth the wait

for this employer.

Bad

Vibrations

This client came to us with a serious problem--a

recent NCCI inspection had assigned a much more

expensive classification to their operations. In

fact, this new classification was so expensive

that they didn't see how they could stay in

business. The client did field testing and

corrections of rotating mechanical equipment,

performing sensitive acoustic analysis of

unwanted vibrations in the equipment, and then

making adjustments to correct the unwanted

vibrations.

We helped this client make their case to the

NCCI appeals board, and the end result was that

most of their field workers were removed from

the expensive millwright classification. The

huge increases in Workers Compensation insurance

premium were thus averted, and the company could

happily continue helping their clients.

SOME

OLDER CASES FROM

OUR FILES

Inherit The Mod

AIM was called in because the insurance company had

turned over Workers' Comp audits to a collection

agency, looking to collect approximately $30,000

from a small masonry contractor. Turns out the

company had been formed when two sons merged the

separate companies that had been owned by their

respective fathers. The fathers' companies had

earned credit mods--experience modification factors

lower than 1.00--because of their good loss history.

But the insurance company had treated the sons'

company as if it were a completely new business.

This was a mistake. When AIM got the NCCI to

correctly calculate an experience modifier for the

sons' company based on the loss history of the

fathers' companies, the resulting experience

modification factor (and the contractor's credit

which they then became eligible to receive)

completely offset the $30,000 additional premium the

insurer had been seeking.

AIM to the Rescue

We recently helped two separate manufacturers who

both had the same classification mistake, even

though they were in different businesses. The first

manufactured a filtration system used by machine

shops and other manufacturers to recycle cutting

oils. The second manufactured lifesaving rescue

equipment used to free motorists trapped in

vehicles. Both of these employers had been in Class

Code 3632, the Machine Shop classification that is

also assigned to a variety of other manufacturers

who do not fit into a more specific classification.

The thing is, both of these employers really did fit

into a more specific classification, because the

products they made were both hydraulically driven.

The proper classification code for such

manufacturers carries a rate approximately one third

lower than the machine shop class. Yet both of these

companies had been in the wrong (and more expensive

class) for years.

Fortunately, AIM was able to correct this mistake by

working with their respective insurance companies,

and these clients ended up receiving significant

lump-sum refunds, along with cutting their current

and future Workers' Comp premiums substantially.

A Classic Example

Often, potential clients of AIM will tell me that

they believe their agent already provides the kind

of scrutiny and review of Workers' Comp premiums

that we do, and so they feel that our services

really aren't needed. This actually isn't so (after

all, every company we've ever produced a refund or

reduction for had an agent) but some employers still

can't be persuaded. But one recent case of ours

illustrates the kind of deeply-embedded mistake that

we often find causing Workers Comp overcharges, and

it also illustrates why agents often can't be

effective at catching and correcting these kinds of

problems.

The trouble for this insured employer started when

the NCCI inspected their operations. The result of

the inspection was to change this employer to a more

expensive classification. Under the rules, the

insurance company was obligated to follow what NCCI

told them was the correct classification. Thus, this

company's annual premiums for Workers' Compensation

insurance were increased by more than a third, all

in one fell swoop.

They asked their agent to help them, as they felt

the NCCI decision was wrong. And the agent did

indeed try to help them, assisting them in

requesting a review by NCCI of this classification

decision. But all the insured's letters (and those

of the agent) were of to avail. NCCI insisted their

classification change was correct, and thus it would

stand, and the insurance company therefore insisted

that it had no choice but to use this more expensive

class to compute premiums.

At this point, the insured employer turned to A.I.M.

After all, since we work on a contingent-fee, they

felt they had nothing to lose.

Our review quickly turned up disturbing questions.

For one thing, when we examined the actual NCCI

inspection report, we found that the inspector's

description of the employer's operations appeared

inaccurate in some key aspects. We tried to point

this out to NCCI (as had the insured earlier) but

NCCI insisted that its inspector had made no

mistake. NCCI further said that, if the insured

wanted the matter resolved, they should use the

Workers' Compensation Appeals Board mechanism that

had been set up in Illinois in recent years (similar

to boards set up in many other states).

We helped this employer prepare their presentation

to the Appeals Board here in Illinois, and we

explained to the board what we felt were the errors

made by NCCI in its inspection. But the Appeals

Board said that the employer had failed to

sufficiently prove that NCCI had erred, and thus the

board did not overturn the NCCI decision.

We here at AIM are experienced with working with the

Appeals Board, and we knew that the board is not the

final word in such disputes. So we encouraged the

employer to appeal the decision of the Appeals Board

to the Illinois Department of Insurance. We also

helped them prepare their presentation to hearing

officers at the Department of Insurance.

The result? The hearing officers reviewed the

material we presented, and the testimony of the

owner of the company, and my own testimony about the

flaws in the NCCI inspection. They also heard from

NCCI. And in the end, the hearing officers

determined that NCCI had indeed erred in its

classification decision. They overturned both NCCI

and the Workers Compensation Appeals Board. In their

ruling, the hearing officers criticized NCCI for its

failings in their inspection of this insured, and

even ordered NCCI to pay for the cost of the

hearing.

This particular case took several years to finally

resolve, but it did indeed have a happy ending (from

the point of view of the insured employer, at

least). And our point is not to criticize the agent,

who did everything a good agent should. Rather, we

just want to explain how some of these mistakes are

just beyond the control and authority of insurance

agents. A.I.M. isn't in business to replace agents,

but rather to supplement their efforts and to

provide a level of specialization and expertise that

typically isn't available to an agent.

By the way, this particular client was a job-shop

precision machining company. For technical reasons,

it appears that it is very common for precision

machining shops in Illinois to be overcharged. For

more information on this subject, check out our

section on Precision Machining & Workers

Compensation in Illinois.

Credit Where Credit

Is Due

When we reviewed the Workers' Comp premium charges

for a good-sized sewer contactor in the Chicago

suburbs, we found the contractor was pretty

knowledgeable about Workers' Comp. They also had a

close relationship with their agent. Yet our review

discovered that they had not gotten the Contractor's

Premium Adjustment Credit they should have on a

policy from a year or two back. They had gotten the

credit on the policy before this one, and on the

policy after this one. And they were very surprised

when I pointed out that they had not gotten the

credit on this particular policy. For this year, the

credit amounted to a substantial reduction in

premium (in the neighborhood of $20,000) and yet

somehow it had not been applied to this particular

past policy.

Needless to say, we're now in the process of

straightening this out, but this illustrates how

things can fall between the cracks sometimes,

particularly with something like the Illinois

Contractors Premium Adjustment Credit. For a related

story on this, by the way, take a look at our

News&Views section.

A Space Case

This case involved AIM producing twin refunds for a

specialized manufacturer in the western suburbs (of

Chicago). Our review resulted in their receiving a

refund of slightly over $22,000 from the insurance

company that wrote their Workers' Comp for the years

1991 through 1996, as well as an additional refund

of $15,000 from the insurance company that wrote

their 1986-1990 policies. (The two insurance

companies involved, by the way, are both large,

well-known direct writers who specialize in writing

Workers' Comp.)

This client specialized in ultra-close tolerance

manufacturing of metal and glass mirrors used in

weather and surveillance satellites (as well as

other optical systems). But in spite having dealt

with insurers who tout their Workers' Comp

expertise, this manufacturer had been overcharged

significantly. And even though NCCI had inspected a

few years ago, the problem wasn't caught because

NCCI misunderstood some aspects of the

manufacturer's business.

We worked to correct the NCCI inspection, and then

worked with the two insurance companies to get the

overcharges returned. The results: a lower

classification approved for future policies, and

significant refunds back from past policies.

The Misapplied

Mod

In another case, we helped a small electrical

contractor get his current Workers' Comp insurer to

rescind a recent large increase in the client's

Experience Modification Factor. On the 1996-97

policy, the Mod had gone from 1.00 (last year) to

1.41 this year, causing a large and unexpected

increase in premium.

When we reviewed the situation, we found that the

insurer had not actually applied that Mod properly.

We worked with the Department of Insurance, and got

the insurer to remove the increased Experience Mod

entirely.

Even though the insured had protested vigorously to

the insurance company when he learned of this Mod

increase, he had been unable to get any relief until

AIM got involved. Even though the Mod was correctly

calculated, the insurance company had not followed

proper procedure in endorsing it onto the policy,

and thus we were ultimately able to get it removed

from the policy.

Appealing the Appeals

Board

Another client of ours received a refund of just

over $36,000 due to our efforts. These refunds

were for the policies running from 1987 through

1995.

This precision-machining shop had been denied

the use of the proper precision machining

classification by NCCI, and assigned instead to

the regular machine shop classification. In

fact, NCCI had inspected not once, but twice,

both times assigning the general machine shop

class rather than the precision class.

Our review uncovered serious problems with both

inspections, and we appealed NCCI's decision to

the Appeals Board here in Illinois. But in spite

of what we felt was a strong case, the Appeals

Board declined to reverse NCCI's decision.

We then appealed the Appeals Board's decision,

taking it to a hearing at the Illinois

Department of Insurance. There we detailed the

problems with the NCCI inspections, and

presented the same evidence as had been

presented to the Appeals Board about the nature

of the client's manufacturing operations.

The result was that the hearing officer ruled

that this client did in fact belong in the

precision machining class (a much less expensive

class than the general machine shop class) and

that the client had properly belonged in that

lower class for a number of years.

Results: a lower classification for all future

policies, and a significant refund from past

policies.

|

Consultants on Workers Comp Classification Codes,

Experience Modifiers, Payroll Audits, & More

|